Höfundur

Gleðileg Jól frá

Egilsstöðum.

24.12.2023,

slóð,

,

Hver selur peningaprentunina, peningabókhaldið til einstaklinga, sem þykjast svo lána fólkinu og ríkinu.

Hringurinn - Tveir jólasveinar? - Jólin 2023

![]() Við erum að reyna að bjarga okkur öllum, og líka okkur gömlu svindlurunum.

Við erum að reyna að bjarga okkur öllum, og líka okkur gömlu svindlurunum.

Alls ekki sprengja upp veröldina, heilmyndina, háskóla leikritið sem við erum leikendur í.

![]() Notum aðferðirnar hans Mandela og klárum kennslu leikritið, heilmyndina öllum til sóma og látum Karlinn með skeggið um dóminn.

Notum aðferðirnar hans Mandela og klárum kennslu leikritið, heilmyndina öllum til sóma og látum Karlinn með skeggið um dóminn.

Það er búið að hringla í tölvunni minni í geymslu diskum og bloggunum á netinu. Sum bloggin eru röng, og koma með annarra skoðanir.

Egilsstaðir, 11.10.2023 Jónas Gunnlaugsson

Velt vöngum, Ef eitthvað er hér sem er til upplýsingar, og til góðs, þá er um að gera að dreifa því sem víðast. Við verðum að læra um fjármálin og breyta svo fjármálakerfinu.

hitt bloggið, slóðin er hér neðan við, bloggin eru tvö,

the path to the other blog is here

000

** **

**

https://jonasg-egi.blog.is/blog/jonasg-egi/entry/2255795/

000

Nikola Tesla var einn af þeim, sem fluttu þjóðunum blessun og leystu fólkið úr ánauð þekkingarleysisins? Þekkingin skapar allsnæktir. Nústaðreyndatrúin stóð á móti Jesú og Nikola Tesla. Við skulum færa Jesú og Tesla aftur inn í skólanna. 20.12.2017 | 18:24 Viðtal við Nikola Tesla 1899

English

24.11.2017 | 22:09

31.8.2018 | 09:28

000

English

7.10.2017 | 13:26

***

Hér er eðlisfræði lífsins 1. 2. 3.

------Jóhannesarguðspjall, Kafli 14, vers 6------

----Velt vöngum um Bíblíuna. Tönn fyrir tönn. Fyrirgefning fyrir fyrirgefningu. EINFALT----

28.12.2017 | 10:06

Þessa slóð verður að lesa.

Learn, learn, learn. Læra, læra, læra.

This link you must read.

My homepage:

hitt bloggið hér neðan við, bloggin eru tvö

http://jonasg-egi.blog.is/blog/jonasg-egi/image/1298552/

Hér er**ég slóð

Og það besta, ég lánaði þér ekki neitt.

**

MYNDIN SEM VIÐ LIFUM Í HOLOGRAMINU ER AÐEINS TIL Í HUGSKOTI OKKAR.

**

Verum fulltrúar gnægta, lausna.

*--- Spuni ---*

****

****

****

**** Fjármálakerfið er einfalt, ekki láta flækja það til að blekkja okkur. ** **

**

The Two Step Plan - Nýtt peningakerfi. Eg. 07.12.2011 jg

****

Nýtt peningakerfi. Eg. 07.12.2011 jg

Islam frá árinu 700 til 2015, mjög fróðlegt.

Það er eins og við getum ekki sagt í orðum, hvert vandamálið er.

**

Skapararnir og Nú staðreynda trúar fólkið.

**

**

**

Íbúðalánasjóður, láttu ekki plata þig.

****

****

Nótur, kvittanir, peningur er færanlegt bókhald.

****

Israel, 29.01.2009. endurtekið

****

**** **** ****

**** **** ****

Israel, 29.01.2009. endurtekið

Snúðu jörðinni og stækkaðu eða minnkaðu með músinni.

Ný nú mynd kemur upp þegar þú endurræsir, ýtir á refresh, (F5).

****

****

Glenna --

Pottur --

MUNA --

********

MUNA, bankar græddu ekkert. --

********

Gerð --

ooo

Mikil blessun Jesaja 9:1-20 ---

****

Bólur, "KLIKK, PIKK, BRELLA, BRELLA."

****

Try to understand the money masters

We must learn a " New World Order "

Peningar eru flutningabílar. ----

Fjármálakerfið, fjárfestar, tæmdu fésýslufyrirtækin -----

****

ENGLISH -

Paper money -- (Stjórnarskrá - peningana -- Constitution - Of money jg) ----

Central-banks ----

Try to understand the money masters

Learn, learn, learn. Læra, læra, læra.

ENGLISH

http://www.herad.is/y04/1/2011-10-05-Central-banks-05.htm

****

****

Verum fulltrúar gnægta, lausna.

**** **** ****

**** **** ****

---- SJÓÐUR "0"

Af hverju talar engin um "KREPPUFLÉTTUNA."------****Ríkisstjórnin**** - -----Kreppufléttan 2013 og miðbankinn--------Kreppu, verðbólgu, verðhjöðnunar fléttan------Getum við skilið hvernig spilað er með okkur?------Jóhannesarguðspjall, Kafli 14, vers 6---- 12 Year Old Girl Paints Heaven, Unbelievable! ---- Hér er sýnishorn af sálum sem eru að koma í stórum stíl inn í "mannheima" til að kenna okkur hinum.---- http://www.youtube.com/watch?v=Xzq4PHJoItU---- Fluga á vegg.----Eignirnar----Kreppufléttan, læra---- Thomas Jefferson sagði okkur þetta allt saman. ----Miscellaneous, Ýmislegt----Dept is slavery Go to the dot “.”Money As Debt The deptindustry It's Not a Deficit, It's New Money ----Ríkisstjórnin----Kosningamálin verða.----icesave-2 - Hótun----Skuldir einkabankanna----Fléttan ----Ámynning - Eignirnar færðar úr fasteigninni yfir í töluna sem bankinn skrifaði í tölvuna hjá sér. ---- Loftpeningar ----Þú elskar að láta plata þig. ----Miðríkið----Merkilegt ----Mjög merkilegt, peningaleikur. ----"Arðurinn" eru eigur fólksins, eigur heimilanna, eigur atvinnuveganna ---- MUNA ----Bóndabær----Restoring our Financial Sovereignty A New Monetary System----Einfalt peningakerfi.----www.herad.is ----http://www.ismennt.is/not/jonasg/jg/jg06/----http://www.herad.is/y04/1/----

Nýjustu færslur

- Hér er hægt að fá að vita heilmikið um það ""hvað varð um pen...

- Ef allir læra um bókhaldið, peningaprentunina og styðja stjór...

- Er heimurinn loks búinn að missa vitið? Úkrainu stríðið hóf...

- " Við erum komin nálægt því að búa til svokölluð krabbameinsb...

- Göng beint á Seyðisfjörð og beint á Mjóafjörð, áfram beint á ...

- Það væri nánast "ómögulegt" að stöðva þróun gervigreindar og ...

- Valgerður tók lyfið Ivermectin, til að forðast Covid-19, lækn...

- Ítrekuð alvarleg atvik vegna hælisleitenda í Fjölbrautarskóla...

- Alls ekki svara þótt hent sé kjarnorku sprengjum, heldur reyn...

- Ert þú syndlaus, villt þú ekki hlusta á þann góða? Hér er ath...

- Nýlega kom hinsvegar í ljós í forklínískum rannsóknum að engi...

- Þetta upphlaup gagnvart Ráðfrúnni er til að við gleymum að fj...

- Verður að skilja, að leiðandi Bolsjevíkar, sem tóku yfir Rúss...

- How the Russian soul can save the American Empire - If we don...

- Munum að fortíðin, nútíminn og framtíðin eru nú, allt er í h...

Eldri færslur

2024

2023

2022

2021

2020

2019

2018

2017

2016

2015

2014

2013

2012

Apríl 2024

Heimsóknir

Flettingar

- Í dag (25.4.): 1

- Sl. sólarhring: 4

- Sl. viku: 36

- Frá upphafi: 169380

Annað

- Innlit í dag: 1

- Innlit sl. viku: 19

- Gestir í dag: 1

- IP-tölur í dag: 1

Uppfært á 3 mín. fresti.

Skýringar

The real truth about the 2008 financial crisis | Brian S. Wesbury | TEDxCountyLineRoad

https://www.youtube.com/watch?v=RrFSO62p0jk

Hér er sagt að ekki má bókfæra veðið hjá bankanum, niður þótt það komi kreppa, og sama þarf að gilda um húseigandann.

In the 1930s, mark-to-market accounting actually took lots and lots of banks out. *

In fact, it was such a bad law

that the SEC at the time told Franklin Delano Roosevelt

that he should get rid of it,

and he did in 1938.

It didn't come back, all the way till 2007.

On March 9, 2009, they announced the hearing,

held the hearing on March 12, changed the accounting rule on April 2,

So, what does mark-to-market accounting do?

000

Smá endursögn á íslensku.

Bókhaldslögin, reglugerðin, reglan, sem setti hvern bankann af oðrum á hausinn 2008 var mark-to-market accounting, það er núsöluvirði eigna.

Í kreppu, vildi engin kaupa neitt, og þá varð bankinn bókhaldslega eignalaus.

Þessi regla var notuð fyrir 100 árum og í kreppunni 1930 var hún sett til hliðar.

Árið 2007 var reglan virkjuð, og þá urðu bankarnir bókhaldslega eignalausir í kreppunni 2008, og allt fór á verri veg.

Þarna urðu 300 milljarða dollara vandræði, sem eru smámunir, að 4 trilljóna dollar vandræðum.

Þingmaðurinn Barney Frank lét breyta bókhaldsreglunni 2.4.2009 og þá fór fjármálakerfið að lagast.

Vandræði bankana voru vegna þessarar bókhaldsreglu, um að nú söluverðmæti eigna væri bókfærð sem eign, og urðu bankarnir þá eignalausir þegar kreppan kom og allt varð óseljanlegt.

000

Textauppskrift

00:00

Translator: Queenie Lee Reviewer: Peter van de Ven

00:07

I'm about to tell you some unconventional wisdom, alright?

00:14

I called my talk today "The real truth about the 2008 financial crisis."

00:21

So, I guess what I ask you to do this morning

00:23

is to think about what you believe

00:27

what the conventional wisdom is about 2008,

00:31

and I'm going to put some words in your mind or describe it this way,

00:35

and that is most people believe

00:37

that the free-market capitalist system, especially bankers, are greedy,

00:45

they go through periods of excess speculation,

00:51

and then the world collapses

00:54

and the government has to come in and save us.

00:58

By the way, this is the story that was told about the Great Depression,

01:02

and it is also the story that is told about the 2008 financial crisis.

01:09

Now, before I get into the meat of my presentation,

01:12

I want you to think about something else,

01:16

and that is that the Federal Reserve

01:19

controls the level of short-term interest rates in our economy.

01:24

Everybody knows that today,

01:26

they're holding those interest rates at 0%,

01:29

trying to get the economy moving again.

01:35

What lots of people don't remember is that back in 2001, 2002 and 2003

01:42

the Federal Reserve dropped interest rates to 1%.

01:45

I want you to think about this.

01:47

Because when you make a decision to take out a loan,

01:50

when you make a decision to buy a house,

01:52

what is the most important ingredient of that decision?

01:56

I mean, obviously, whether you have income,

01:59

whether you like the house,

02:00

but one of the most important ingredients of that

02:03

is the level of interest rates.

02:05

Alan Greenspan pushed interest rates

02:08

down to 1% in 2003 and 2004.

02:14

In fact, interest rates were below inflation

02:18

for almost three years - below the rate of inflation.

02:23

Now, how do you think about this?

02:25

So, when you're looking at a house - can I afford this house, the payment?

02:29

Obviously,

02:30

those payment streams are determined by the level of interest rates,

02:33

and when interest rates are low,

02:35

you're going to buy a bigger house,

02:37

you're going to buy in a better neighborhood,

02:39

buy cherry cabinets and granite counter tops

02:41

because you can afford it.

02:43

So, let me put this into a story that I know you can understand.

02:48

And that is, when you come to a green light in your car -

02:54

you're driving along, there's a green light -

02:56

how many people in here actually have ever stopped at a green light?

03:03

I'm not talking about senior moments.

03:05

(Laughter)

03:06

I'm talking about stopping at a green light,

03:09

getting out of your car and walking around to the other side,

03:13

just to make sure the other one really is red

03:17

Because, obviously, if it was green too,

03:20

it'd be dangerous to go through that intersection.

03:23

So what happens when Alan Greenspan or the Federal Reserve

03:27

holds interest rates all the way down at 1%?

03:30

You get a green light.

03:33

You get a green light to make a purchase

03:35

that's bigger than probably you should,

03:38

and by the way, the financial system is no different than you.

03:42

Bankers, they're no different than individuals.

03:46

They would say, "Hey, with interest rates so low,

03:48

leverage, borrowing doesn't matter as much, it's cheap.

03:52

So, why don't we lever up a little bit more?

03:55

After all, it's Alan Greenspan, the smartest man in the world,

04:00

that tells us interest rates are 1%;

04:02

in other words, all the lights are green."

04:06

And, so what happens when you hold interest rates down like this?

04:10

You cause people to make decisions that they wouldn't otherwise make.

04:14

Now, let me put this in a different perspective.

04:17

House prices went up 8% in 2001.

04:23

By 2004, 2005

04:26

they went up 14% in 2004, 15% in 2005.

04:31

So you could borrow at 1%, especially with those teaser loans,

04:36

and you could have a house that was appreciating at 14%:

04:40

what a great deal!

04:42

And, so what happened is we encouraged more people to buy homes,

04:46

bigger homes than they should have at the time.

04:50

We also encouraged bankers to take on more leverage,

04:54

and make more risky bets than they would have

04:57

if interest rates were higher.

04:59

In fact, if interest rates would have been 4 or 5%,

05:02

I don't believe we would have had the housing bubble at all.

05:06

Now, let's go back in time just a little bit,

05:09

because this has happened before.

05:11

The last time the Federal Reserve really held interest rates too low for too long

05:17

was back in the 1970s.

05:20

In the 1970s, farmers bought too much land,

05:23

we drilled too many oil wells,

05:26

we were betting on oil prices going up forever,

05:29

and in the 1980s, when farmland prices collapsed and oil collapsed,

05:33

banks collapsed too.

05:35

By the way, the entire savings and loan industry

05:38

also collapsed in the 1980s

05:40

because of the same reason:

05:41

they made too many loans when interest rates were low,

05:45

and then, when interest rates went up, they collapsed.

05:48

At the same time,

05:49

we made big banks make huge loans to the Latin and South America.

05:54

And so, if you go back and look at the 1970s, banks expanded,

05:58

they made loans to farming, housing, oil, Latin and South America,

06:03

and all of those parts of the economy collapsed

06:06

in the late of 70s, early 80s,

06:08

and the banking system was in monster trouble.

06:12

In fact, the eight biggest banks in America in 1983 had no capital -

06:19

zero capital -

06:20

because they had lent too much to Latin and South American countries

06:24

that all collapsed.

06:26

And here's my point of going back to that.

06:29

That is if you go back and look at the 1980s,

06:32

the problems of the 1980s - the banking problems -

06:36

did not take down the entire economy.

06:39

This time, they did.

06:42

And so, the question is why,

06:44

and we're going to deal with that in just a minute.

06:47

And so one of the things that I want to do

06:49

is tell you something I just did, right?

06:53

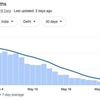

This is the picture of the S&P; 500 -

06:56

the 500 largest companies in the US stock market.

07:00

It's a picture from 2008 all the way through the first half of 2009.

07:06

What I just recently did is I went back,

07:09

and I read the verbatim transcripts

07:13

of all the Federal Reserve meetings during 2008.

07:19

Now, the reason I just did this

07:21

is because they only come out with a five-year lag.

07:23

The Fed they released little statements,

07:25

and then minutes,

07:27

and then five years later,

07:28

they give us the full transcripts of what they've talked about, right?

07:32

All of those red dots, there's 14 of them, are a Fed meeting.

07:38

Normally, the Fed has six or seven meetings,

07:40

but that was a crisis year, right?

07:42

And so the Fed had 14 meetings that year.

07:46

Just to put this in perspective,

07:48

it's 18 or 20 people sitting around a table,

07:51

and the verbatim transcripts are each of them talking

07:54

for three or four minutes

07:55

if they go around and they vote and they go around again; they vote.

08:00

These transcripts were 1,865 pages long,

08:05

559,000 words.

08:09

Now, I read these for you, just so you know.

08:12

(Laughter)

08:13

And some people have a hard time, like, what is 559,000 words?

08:18

Well, the Old Testament is 593,000 words.

08:23

I mean think about that,

08:24

we've built the universe,

08:25

wandered around the desert for 40 years, 50 years,

08:28

built an ark ...

08:30

There is a lot of stuff that happened in the Old Testament.

08:33

(Laughter)

08:34

The Fed used that many words

08:37

for one year of US economic history.

08:42

Now, I could head down this road -

08:44

maybe that's another TED talk - because that's one of our problems.

08:48

Nonetheless, one of the things I want to point to

08:51

is this huge decline in the market

08:54

that happened in September and October of 2008.

08:58

You know what happened in September and October of 2008?

09:02

Well, first of all, the bloody weekend, September 13th, 14th, I think it was,

09:07

when Lehman Brothers failed, AIG, Fannie Mae, and Freddie Mac,

09:12

and all of those things happened,

09:14

and the Federal Reserve started a program called quantitative easing;

09:18

that's where they started to buy bonds and inject cash into the economy

09:22

in an attempt to save us.

09:25

At the same time, in fact, just a few weeks later,

09:29

on October 8th of 2008, Hank Paulson, the Treasury secretary,

09:36

President Bush, the Bush White House, Congress passed TARP:

09:42

the Troubled Asset Relief Plan,

09:44

and it was 700 billion dollars of government spending

09:48

to save our banking system, okay?

09:51

I want you to take a look at this chart a little more closely.

09:55

Quantitative easing started right here, TARP was passed right there.

10:01

Did it help?

10:04

In fact, the worst part of the crisis was after TARP was passed.

10:09

The stock market fell 40%;

10:12

financial-company stocks fell 80% after TARP was passed.

10:18

In fact, if I look at this chart and kind of squint at it,

10:21

look at all those red dots,

10:22

I would say the more the Fed met, the more the Fed did, the worse it got.

10:28

So, something else must have been going on, right?

10:33

In my opinion,

10:35

the government did not save us,

10:37

and in fact, this is one of the problems that people have

10:40

when they're trying to understand the economy.

10:43

You see, there's an interesting fact about our world, and that is

10:47

the free market - capitalism -

10:52

does not have a press agent;

10:56

the government does.

10:59

The Federal Reserve does.

11:02

In fact, there are about 2,000 books about the financial crisis,

11:05

but there are three main ones that have just come out.

11:08

One is by Timothy Geithner,

11:09

former Secretary of the Treasury under President Obama.

11:13

He was the head of the New York Federal Reserve Bank during 2008.

11:20

He'd written a book about the crisis;

11:22

who do you think he says

11:24

saved the world?

11:25

(Laughter)

11:27

Timothy Geithner, of course.

11:29

Ben Bernanke.

11:31

He doesn't have a book out - he has a book of speeches out -

11:33

who do you think he says

11:35

saved the world?

11:37

Ben Bernanke.

11:39

Hank Paulson has a book out,

11:41

and who do you think he says saved the world?

11:43

Hank Paulson.

11:44

In fact, it's not really that they take credit themselves,

11:47

but they credit TARP

11:49

and quantitative easing and stress tests;

11:52

that's what Timothy Geithner takes credit for:

11:55

stress testing banks, so that everybody can trust them, right?

11:59

This is where I want to shift gears, just a little bit,

12:03

because what I want to tell you is why - or explain -

12:08

is why I believe this banking crisis

12:12

turned into a true overall economic crisis,

12:16

while if you look back in the early 1980s,

12:19

where banks had more losses than they did in 2008,

12:23

the economy did not collapse,

12:25

and in fact started to accelerate without TARP,

12:28

without quantitative easing.

12:30

In fact, Paul Volcker was raising interest rates in the early 1980s,

12:34

and the economy recovered.

12:36

Here we cut interest rates to zero,

12:38

and the economy has grown relatively slowly.

12:41

So, what caused this problem?

12:44

By the way, in those transcripts that I said that I read,

12:47

Ben Bernanke asks his staff to go out and find out how big the problem is,

12:53

how many subprime loans were made,

12:56

how many losses could we face,

12:58

and he has a staff of about 200 Ph.D. economists,

13:03

and they came back with a number of 228 billion dollars.

13:07

Now, don't get me wrong,

13:10

I'd love 228 billion dollars, right?

13:13

But 228 billion dollars is small compared to a 15 trillion dollar economy.

13:19

So, how did that small problem turn into a problem

13:24

that almost took down a 15 trillion dollar economy,

13:27

and the answer is mark-to-market accounting.

13:31

It's a little-known accounting rule

13:33

that most people know nothing about, right?

13:37

It was put into place in November 2007

13:40

after being out of place, not enforced, since 1938.

13:45

Now, let me give you a little bit of background on an accounting.

13:50

In the 1800s, bookkeepers,

13:54

they were bookkeepers.

13:56

They weren't the accounting profession yet.

13:59

They were getting more and more sophisticated,

14:01

but they usually marked everything to market.

14:04

So, if you think about this,

14:05

if the farmland goes up in value, if your machinery goes up in value,

14:09

if your inventory, if loans go up in value,

14:11

you get to mark those up.

14:13

So, in good times, things look better,

14:15

but then, when you start marking things down, things look worse.

14:19

And I believe that if you go back to the 1800s,

14:21

this is one of the reasons why we have very sharp dips and drops in the economy,

14:26

panics and depressions

14:28

and things like that.

14:30

In the 1930s, mark-to-market accounting actually took lots and lots of banks out.

14:36

In fact, it was such a bad law

14:38

that the SEC at the time told Franklin Delano Roosevelt

14:41

that he should get rid of it,

14:43

and he did in 1938.

14:45

It didn't come back, all the way till 2007.

14:48

So, what does mark-to-market accounting do?

14:51

Well, let me give you a story.

14:53

Just imagine you live on the coast of Texas, in Galveston, Texas,

14:59

and you have a $500,000 house right in Galveston, near the beach,

15:05

and you have a $300,000 mortgage,

15:07

and there is a hurricane on the way.

15:10

And it's only four or five hours away,

15:12

and they've told you to evacuate your neighborhood,

15:16

and you're packing up your pictures,

15:18

you're packing up your most important belongings,

15:20

and just before you leave the driveway, your banker shows up.

15:25

(Laughter)

15:26

And your banker says,

15:27

"You have a $300,000 mortgage on this house,

15:31

and there's a hurricane coming.

15:33

Your house is about to be destroyed.

15:35

We're really, really worried about our loan.

15:37

I know you've paid every payment,

15:39

but we're going to have to mark this house to market."

15:43

And you're like, "Well, everybody's gone, no one left.

15:45

I saw the realtor leave. Who's going to bid on this house?"

15:49

He said, "Don't worry, there's a fire truck.

15:51

Let's get the fireman to bid on it.

15:54

They stopped the fire truck, said, "Hey, make a bid on this house."

15:57

Fireman says, "There's a hurricane about to hit.

16:00

I'll pay 20 grand for it,"

16:02

and the banker says, "You know what, you owe me $300,000,

16:05

but the house is only worth $20,000

16:07

because that's the bid.

16:09

So, if you can't come up with $280,000 dollars right now,

16:15

you're going to lose your house.

16:17

You're bankrupt.

16:18

That's what mark-to-market accounting is.

16:21

And so in 2008, what we did is we said -

16:24

what people were doing is -

16:25

they were saying a hurricane is heading, that no ones are worth nothing,

16:29

and so, banks couldn't sell assets, they wouldn't buy assets,

16:34

and in reality, what happened is their losses spiraled out of control,

16:38

and it turned to a $300 billion problem into a $4 trillion problem.

16:45

Now, the amazing thing is, right at the bottom,

16:49

March 9, 2009,

16:52

something changed the world.

16:54

There's a little-known - well, actually he's not little-known,

16:57

but he's retired now - Congressman named Barney Frank.

17:01

His financial services committee actually held a year,

17:04

and he brought the accountants in

17:05

and said, "We don't think this rule is right,"

17:08

and they changed the accounting rule.

17:10

On March 9, 2009,

17:12

they announced the hearing, held the hearing on March 12,

17:15

changed the accounting rule on April 2,

17:17

and from that point on, the economy has grown;

17:20

the stock market is up 200%.

17:23

And, what I'm getting to here is the fact

17:26

that I believe this crisis was not generated by over-speculation,

17:33

well, in fact, was caused by the Federal Reserve in the first place,

17:37

and by changing this accounting rule,

17:39

we brought about a recovery in our economy that most people don't understand.

17:45

What they do believe

17:46

is that the government has caused the recovery,

17:50

especially the Federal Reserve through quantitative easing.

17:53

I want you to think about this for one second, and then I'll close.

17:57

That is that what the Federal Reserve does is they go out and buy bonds,

18:02

and when they buy bonds, they inject cash into the banking system,

18:05

and typically, banks will take that money and lend it out,

18:09

but in the last five years, banks haven't.

18:12

What banks have done is they've begun to sit on excess reserves.

18:15

And so, when you look at the economy today and see how it's growing,

18:20

what's fascinating about this

18:23

is that this growth is actually coming from entrepreneurship.

18:28

I want you to remember one thing,

18:30

and that is Ben Bernanke and Janet Yellen have never stayed up all night

18:36

drinking Red Bull, eating pizza and writing Apps;

18:41

(Laughter)

18:42

they've never fracked a well;

18:44

they haven't ever built a 3D printer.

18:47

And so, when you look at our economy, what I'd like you to do is have faith

18:52

that the free market actually works,

18:54

and realize that many many times,

18:56

government, rules, regulations and actions,

18:59

especially with interest rates, have major impacts.

19:03

I think the understanding of 2008 that people have, the conventional wisdom,

19:08

that banks lost control is actually the wrong thing.

19:12

I believe it's government that lost control,

19:15

and by fixing that rule,

19:17

we actually started the recovery that's underway.

19:20

Thank you very much.

19:21

(Appla

Egilsstaðir, 03.11.2019 Jónas Gunnlaugsson

Þarna urðu 228 milljarða dollara vandræði að 4 trilljarða dollara vandræðum, þegar hugsanlegt núsöluverð eigna var bókfært sem verðmæti eigna bankana. Þá fóru margir bankar á hausinn, og Bandaríkin björguðu mörgum, en ekki þeim íslensku.

Bloggar | Breytt 31.3.2020 kl. 23:59 | Slóð | Facebook | Athugasemdir (0)

Bloggar | Breytt 31.3.2020 kl. 23:59 | Slóð | Facebook | Athugasemdir (0)